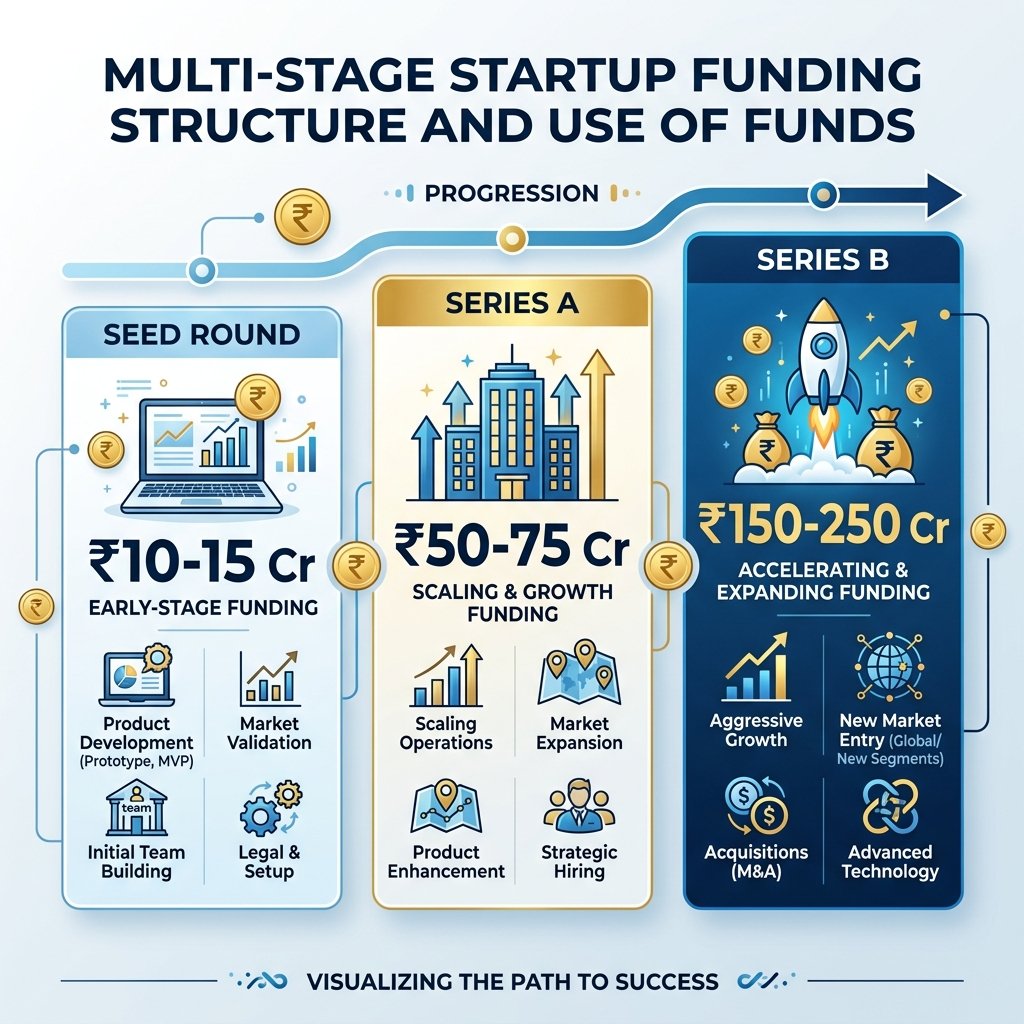

1. Capital Foundation

Initial Investment & Deployment

A structured approach to capital allocation, beginning with our immediate China R&D prototyping budget and scaling into a 5-year pan-India deployment strategy.

Phase 0: Immediate R&D Budget

We are executing a highly optimized immediate prototyping phase to validate hardware and local software integration during the 30–40 day Shenzhen sourcing sabbatical.

Seed Round: ₹16.00 Cr

Y1 CapEx: ₹4.30 Cr

Y1 Team: 39 FTEs

5-Year Capital & Deployment

Total equity funding of ₹111 Cr across three rounds to reach Pan-India scale — 400 kiosks, 85 pods, 22 mobile units, and 290 FTEs.

Total Funding: ₹111 Cr (Seed + A + B)

5-Yr CapEx: ₹8.00 Cr

Y5 Revenue: ₹319.04 Cr